The world is changing before our very eyes

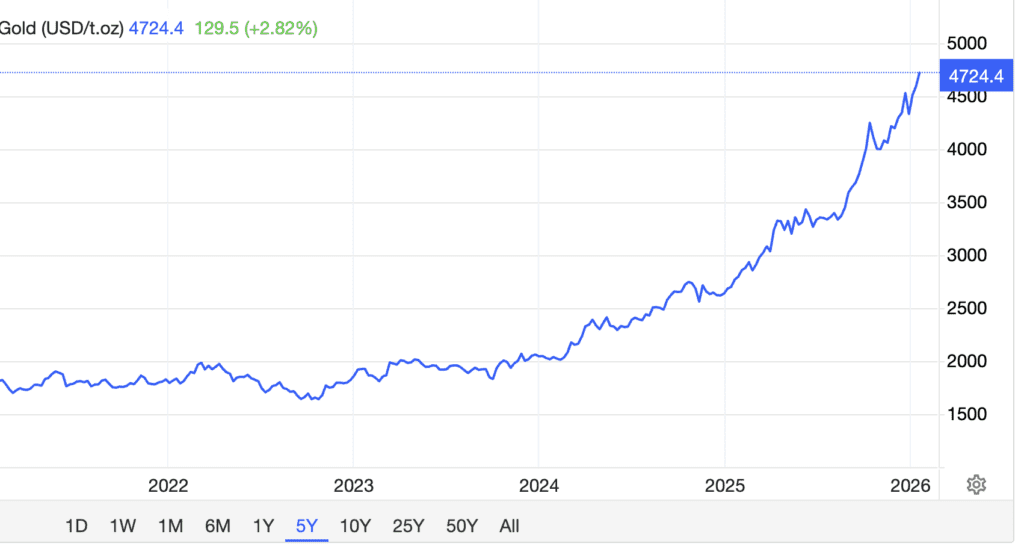

Conflict is spreading across the world, with economic instability as a backdrop. No wonder gold is doing what it’s doing.

Are we on the cusp of a bigger change, of a reset of sorts? If so, what are the implications for us as investors?

We discussed this with together with Chris. He laid out his thesis and how he is adapting.

Diversify your sources of information

When governments and the powers that be start to lose control of the narrative, they start clamping down.

We see it in the UK where thousands of people are sitting in jail over posts on social media and where elections are being cancelled.

We see it in Australia, where they passed a patently totalitarian law called the “Combatting Antisemitism, Hate and Extremism Bill 2026.” The law allows for people to be jailed for causing others to “feel fear,” with room for broad interpretation.

More information on this law here.

How is this relevant to investing?

- Western democracy and institutions are decaying, but assets in these jurisdictions still command a premium as if nothing’s wrong.

- Writing about anything, or commenting about the news, is increasingly fraught with risk. This means the quality of journalism and research will decrease as well.

Unpalatable media is already banned throughout the West, such as Russian news and Iranian news, more specifically their TV channels. Click these links here and see, maybe even the websites don’t work in your country.

Chris’ newsletter is interesting in this regard as it challenges conventional perspectives but still complements mainstream analysis. You don’t need to agree with him on everything (I don’t), but you should at least understand where he’s coming from.

Use our affiliate link for a significant discount and 30 days satisfaction guaranteed.

To a World of Opportunities,

The Wandering Investor.

Subscribe to the PRIVATE LIST below to not miss out on future investment posts, and follow me on Instagram, X, LinkedIn, Telegram, Youtube, Facebook, and Rumble.

My favourite brokerage to invest in international stocks is IB. To find out more about this low-fee option with access to plenty of markets, click here.

If you want to discuss your internationalization and diversification plans, book a consulting session or send me an email.

Transcript of “Investing in an Age of Conflict – 2026 Update”

LADISLAS MAURICE: Hello everyone. Ladislas here from The Wandering Investor and today I’m with Chris who manages a hedge fund and a very interesting newsletter I subscribe to. And we’ll be discussing investing in an age of conflict. Chris, how are you?

CHRIS: I am well. I’m well, thank you.

LADISLAS MAURICE: So, we did a video about a year, a year and a half ago on this very topic, investing in an age of conflict. And I feel like the situation has not improved, we’re seeing more and more conflict. It’s absolutely insane right now, there’s no international law anymore. People just do whatever they want to do. You never really know what’s coming next. So this uh investing in an age of conflict theme is ever more relevant. So what are your what are your thoughts on this, Chris?

CHRIS: If we go back and we think about how we’ve been thinking about this for the last few years and possibly we discussed it, I can’t actually recall exactly the conversation we had roughly a year ago, but I’m pretty sure um, I’ve got the basis of it because there’s none of this is particularly new to us.

The conflict that we’re seeing is very predictable. It’s predictable as a consequence of economic realities. And so it wasn’t difficult for us some years back to um to identify the probability or even it’s more than probability, I guess. It’s it’s like at some point it’s it’s inevitable. I would say the inevitability of the conflict that we are seeing was um was baked in the cake. And it’s baked in the cake as a consequence of economic reality. So we’re just further down that particular path now. It will continue until we have a restructuring of the world. And that’s going to restructure around economics and as a consequence, politics. The two are tied, they always have been. And what we what we’re watching now is a conflict for uh dominance in the in the sort of global arena, if you will.

And so but back to the sort of predictive nature here, um it’s not that like I’ve got crystal balls, I don’t, I got two and neither are crystal, but it’s pretty obvious that when you have these economic situations such as the debt, but they’re golden.

LADISLAS MAURICE: But they’re golden.

Debt crisis implications for socialist economies

CHRIS: Yeah, the debt situation on top of the social liabilities that have been built into the Western system in particular. Those again are all liabilities. It’s not merely a liability that sits on a balance sheet. It’s a liability that sits within a societal structure. And that’s an important definition to understand, because it’s not merely a default that can wipe out that particular debt. In other words, for example, let’s just say you have a country as we have had in many instances in the past, say in Latin America, in many of the countries that you have spent some time in if we look at the emerging market world, you’ve had debt defaults and we’ve had restructurings in these countries. And very often, not always, but very often where you don’t have a socialist structure underpinning that or or as a as a component of it, the social fabric of that society doesn’t disintegrate.

In other words, when there aren’t liabilities, you know, things like pensions and obligations, health care, education, yada yada yada to the citizenry who have become accustomed to it, when those don’t exist, or they exist to a lesser degree, and at the same time your governments have built up a debt system and then they collapse, they land up inflating the currency, etc, and devaluing the currency, as a consequence, sure your your citizenry are harmed by that. But they don’t fragment and break apart in the same way as as is more probable when you have the opposite, which is basically like Europe on par excellence today. Massive socialist structure, which is underpinning their economy, which is in itself imploding under green scam, on under increasing bureaucracy and increasing debts. And they and the the the politicians in power are understanding of this, which is why they’re going to war, because it’s a justification that’s required to a distract the citizenry from the the reality on the ground. And B, it’s also a an ability to um eradicate those debts. And so we we can’t, we you know, we can’t because we’re at war, we can’t do X, Y, Z and we need to dedicate this and justify the the debt collapse.

So again, and this is historical, you can go back and you can look through previous previous parts of times of history where the same has been true. So again, nothing particularly, you know, I’m not that smart a guy that I, you know, come out with these things. It’s merely just looking at patterns of history, looking at economic structures and then looking at probabilities of that taking place. And for my job, of course, it’s a matter of then allocating capital to both profit from that and to protect oneself from the fallout.

Western dominance in Latin America and Argentina

CHRIS: And so here we are today, where we are another year down the path and certainly 2026 is off to a spicy start. So there’s a lot going on, Ladislas. I know you’re spending a lot of time in Latin and South America and you’ve got an event down there in Argentina, where we’re very, very heavily invested and increasingly heavily invested, um for a multitude of reasons. But that entire region is also going to go through a restructuring. Um partly as a consequence of the West needing to dominate supply chains and resources, the the Monroe Doctrine 2.0, if you will. And that’s going to have significant consequences to the various economies. And certainly there’s no there’s no country within that region that I can think of, which is probably more that’s set up to be more benefited and and chosen as a party than Argentina.

And you can argue about whether you want that or not, that that’s irrelevant. Um but that’s there’s a huge bullish situation that’s been developing actually for some time there and we’ve been pretty heavily invested through RS Management company and then of course through private equity as well through um another company I’m in involved in.

So, and then part of that all plays into that whole geopolitics, um to some degree it’s also why we’re watching what’s happening in Venezuela. That’s why Greenland’s important. You don’t get to play you you don’t get to choose what’s going to happen in the world, you just get to play alongside and these trends are unfolding and they’re unfolding rapidly and quite violently. So it’s a matter of trying to keep your head about you at the same time as intelligently allocating your capital.

And I would say for one thing certainly that’s I’ve been suggesting for some time for people to get their head around, it’s that the world that we’ve lived in for the past 40 even 80 years is not the world that we’re either actually even in and not the world that we’re moving rapidly into.

Debt and equity markets under geopolitical uncertainty

LADISLAS MAURICE: So, Chris, apart from Argentina which comes with its own set of risks, what are some of the other ways to play this?

CHRIS: When you have chaos, things move like you have geopolitical uncertainty. Geopolitical uncertainty is generally very, very bad for bond markets. It can be bad for equity markets, dependent on the jurisdiction, but just yeah, in general uncertainty is not a particularly good thing. The counter balance to the uncertainty and the um and the negative implications on an equity market in this instance are debt devaluation. That typically historically has been an um inflationary type of outcome. And so equities aren’t necessarily something you would want to be short, um but it is it is kind of geographically important to look at that.

In other words, for example, at the moment the United States has got a massive amount of capital that’s been pouring in both from external as well as domestic. In the United States, it’s all been concentrated largely in the top 10 companies within the S&P. That’s certainly a bubble. It’s one that we’re hedged against in our asset management company. So we we have no interest in being anywhere near that. In fact, we have very, very few positions within the US, because the value simply doesn’t lie there. Where we see opportunity, by and large, is in hard assets. We are moving into an environment, I believe, which is going to be much more a question of return of capital than a question of return on capital. And so when you change that framework in your mind and you say, what gives me that level of underlying stability? That is why we’ve been watching precious metals doing what they’re doing.

Precious metals and commodities will outperform

CHRIS: That’s going to that’s part of a capital rotation cycle, which um we’ve had in the past before and I believe we’re going through now. So the entire commodity sector on a relative basis is likely to outperform broad equities. So that’s and that’s and that’s even through to things like copper. And people will often say, well, copper is like, you know, it’s Dr. Copper and it it reacts to economic growth or the lack of. It can, just like many other commodities, also react to a lack of supply and broken supply chains and so on and so forth. And that’s the geopolitical conflict world that we’re in.

Supply chains in an age of conflict

CHRIS: So back to the conversation that we had about a year ago, how do you invest in a world of of increasing conflict? Supply chains matter. Supply chains are going to be fought over conflict there’s going to be conflict around them. It’s a stagflationary environment. And people will often look at it and go, oh, this is demand destruction, we’re not going to have X, Y, Z. That can be true to some degree, but often what you’re actually having at the same time is a supply destruction. If your supply destruction overwhelms your some demand destruction, you can still have prices go up. So that’s pretty much broadly the environment we’re in is a stagflationary environment. Hard assets are the are the um the places that one needs to be more focused on. And then on a geographical basis, there’s pockets of the world which are far more attractive than others. We we see value in places like China. We see value certainly as I’ve mentioned in Argentina. We’re increasingly looking at we haven’t taken a position yet but Chile and Brazil we’ve got some small positions in.

Why investing in Europe is a bad idea

CHRIS: And the bigger part is often looking and saying, well, what would you not own? And what we would not own is basically on a geographical basis, Europe. Europe’s toast it’s stuffed. I think we’re going to have capital controls before the end of this year. We already have capital controls. They’re simply not called that. They’re masked under the the guise of KYC and AML and regulatory approvals and yada yada yada. But they are capital controls nonetheless. And we see that accelerating. Again, all of this is predictable as a consequence of economic realities. It’s a numbers game. Um and a probability game. So people kind of often get caught up in the narrative and they get caught up in the, oh, this politician’s coming in and that, like none of that shit matters. At the end of the day, none of it matters. Economic reality overwhelms all of that.

LADISLAS MAURICE: Yeah, so you mentioned Europe is not being very uh investable. It’s a hard to disagree with you. They’re literally making bad. Yeah, bad move after bad move. I mean, at this stage, it’s just mostly a a lifestyle play, really. You so you so you said some regions that you’re interested.

Investing in China as a Westerner

LADISLAS MAURICE: You mentioned some parts of South America, fine. You mentioned China. I mean, I’d argue with you, Chris, that, you know, with a Western passport, you probably don’t want to invest in China. Um because it’ll just backfire because of your own government’s actions against China. The way it backfired on a lot of us who invested in in Russia.

CHRIS: Yeah, okay. So, I’ll address that with this. Firstly, China’s not Russia in so far as it’s the largest economy in the world. Sanctioning China is not quite the same as sanctioning Russia. That being said, the politicians in the West who for the most part are simply podium donuts. That’s needs to be clear. And it should be clear to anybody who’s lived through the last five years that the the politicians that we are voting for are not the actual people in power. They have handlers. Um that that seems obvious.

In any event, the point is they may easily take and make decisions that are contrary to our investments, for example, like they did with Russia. But the way to invest and the way to build any portfolio, and this is where portfolio construction makes a is super, super important. And people don’t spend enough time on it. And I realize they don’t because it doesn’t get clickbait. It’s not that interesting, but it is any investor that’s worth their salt, like I wouldn’t, you know, I think I’ve got lots of hedge fund buddies and that, like, this is super important, it is portfolio construction. So within that, you can identify something like China, for example. And the question you have to ask yourself is what are the risks? Fine, we’ve identified one of them, which could be a seizure of assets, it could be a sanctioning of that particular country as a consequence of your own passport, domicile, et cetera, et cetera. That’s fine.

The question then is, is that priced into the market? If it is priced into the market, now you have a baseline. Now, it could be priced into the market to the degree that it’s absolutely 100% going to take place, or or like 90% going to take place, right? And that may not transpire in terms of reality. Reality might be that it’s a 50/50 chance. And as a consequence, the valuation of those assets that you’re buying is going to be severely discounted. That is a trade purely mathematically, on a probability basis that you should make. But it’s not a trade that you make and you put all your money into it. You don’t go 100% into it. You go in with 2%, 5%, something of that nature, right? If you keep making those sorts of bets which have asymmetry on your side, your returns reflect it. That’s been the experience that I’ve had for all my my professional life. And it’s one that basically is the basis to our portfolios that we run. It’s not so much that China might have the West sanctioning them, is that priced? If it’s priced, and it’s priced to a degree where now the assets are significantly cheaper than they could be in any other place, then it’s a matter of now what is your position sizing on what can be an asymmetric bet. So that’s it. And certainly we we saw, gosh, what are we? 26 already?

Will China end up like Russia under sanctions?

CHRIS: Um I think it’s 20, 2023 was when the the Chinese market really got smacked. And and what you saw was institutional Western institutional capital fled, which left asset prices um very attractive. And it fled based on that assumption that, hey, it’s going to be like Russia 2.0. Again, China has way more clout than Russia on multiple fronts. So it’s not that it wouldn’t happen, but it’s that China has a lot of tools it can pull out of the the toolbox to address that. And um and so the West knows that to some degree. So I think the probability of that is actually far lower than it was with Russia. There wasn’t that much that the Russians could do. There’s a lot that Chinese could do to mitigate that or to return a blow on that front. So again, then it’s just matters in terms of what’s the price of the assets, what can you buy them for, what’s the probability and so on and so forth. So that’s where we see some value. Again, it’s a position size question more than it is anything else.

LADISLAS MAURICE: Thanks. And what are your thoughts on Africa, Southeast Asia, Central Asia?

CHRIS: Look, I think the world’s gonna split. It’s already splitting to some degree into hemispheric control. I’ve spoken at length on other podcasts and in our publication around the fact that um and this was pre-Trump that we would start to see a consolidation of the North South across the US. So all the way from from Greenland through to Canada down to Argentina, we would look at we would watch and see the US exerting more political and economic and military influence there to secure those supply chains to basically secure that hemisphere. That was going to have a number of ramifications for various countries within the region, some positive, some negative. Part of it is why Argentina’s doing what it’s doing and we’re very heavily invested there.

Chinese influence in Southeast Asia

CHRIS: The other side of that where you talked about say Southeast Asia, all the time being, I think it’s going to be left alone in so far as they will increasingly be tied to China. Um and they will be allowed to be increasingly tied to China because the West has to recoup before it can try and attempt to go and take that gain that control. That’s what it’s doing at the moment, that’s partly what Venezuela’s about. It’s also why Trump is is sort of stepping out of NATO and that to some degree because it’s like let them deal with it, we’re going to consolidate this.

Mackinder’s Heartland Theory

CHRIS: And then the ultimate game, of course, is to secure Russia’s assets. That’s what the war’s always been about, it’s been trying to obtain and secure what was um originally called Mackinder’s Heartland. So people can look up Mackinder’s Heartland theory. And that was that has been the basis to US foreign policy ever since World War II. And so that hasn’t gone away, it’s just in remission for the time being, such that the US can consolidate north south. And it’s and the reason that it’s needing to consolidate north south is because China in particular has been used the word infiltrating. They have been investing into those regions and securing port deals. You you would know this, Ladislas, whether it might be Nicaragua through to Panama, Colombia, um and Venezuela’s a big part of it. It’s not even just about oil, it’s about a lot of the uh rare earth metals, which get shipped out of Colombia, processed, put on ships in Colombia and shipped out to China. That entire supply chain is why Trump is going after Colombia. It’s why he’s going after Venezuela. It’s not even so much about securing those assets, it’s as as much as it is about ensuring that China can’t secure those assets, right? So so there’s there’s two components to it. But so that that’s that’s going to catch them and they’re going to be sort of caught up in that.

Economic and geopolitical future of Venezuela

CHRIS: I there’s there’s a couple of things that could transpire with respect to Venezuela, um we’ll have to find out what they look like. But we are at war. Um China, Russia, other parties, certainly it would be, I guess, in their interests to see Venezuela turn into a bit of a clusterfuck, such that they can keep if you and I were China and we wanted to defeat our enemy, we would fund a few guerrilla groups to just go there and bomb some pipelines and just disrupt trade and put a premium on any of the oil that comes out of Venezuela, which by the way, I don’t think it’s going to transpire.

We’re looking at up to about $180 billion that needs to be invested to bring infrastructure back up so they can get up to 3 billion barrels a day and that’s not going to happen. It’s not going to happen without massive security guarantees and basically um the US taxpayer funding that, which would basically then be a socialization of expenses with a privatization of the resources. That in itself is going to drive more inequality, it’s going to drive more debt, and it’s going to accelerate the collapse of the Western system over that that can take some time. But structurally, that is what’s most probable.

So Venezuela is more likely to be a problem, um because everyone outside of the US wants it to be a problem. It benefits Russia for it to be a problem, it benefits China for it to be a problem. Vietnam 2.0 would be absolutely perfect for those interests. Basically, if we can’t have it, you fucking can’t either. Which of course was what what uh the US was saying was you, you know, we don’t want you to have it. We’re going to cut off that supply. This is the age of conflict, that sort of age of conflict means the broken supply chains, means increasing um geopolitical conflict and those wars won’t just get fought on a kinetic basis domestically, they’re going to get fought in financial markets, which we’re watching, sanctions, restrictions on movement of capital. All of those things are going to be prevalent.

So I think it’s a very important time for I guess most of your listeners might be, shall we say, Western domiciled at least to some degree. You can’t move some assets out of where you are fast enough. It’s not to say you know exactly where to send them, but it’s a matter of um diversifying risk across probability and relatively good regions. Southeast Asia, as a general, I think it’s going to be fine. There are some cheap assets, um Malaysia’s not particularly expensive, but it depends on what you’re doing and whether you’re doing it in private equity or whether you’re doing as you do in real estate, or whether it’s in equity markets. There’s there’s opportunities in in all of the above.

Capital controls in Europe

LADISLAS MAURICE: Yeah, and I’d like to emphasize this, particularly for Europeans. I mean, capital controls are going to be coming to Europe first, not to the US, not to Australia, not to Canada. It’ll be in Europe first.

CHRIS: And possibly and and when you say Europe, I I include UK and that. Some people sort of include it in that bucket, others don’t. So I’ll make that point. The UK is probably, I think the first out of the gate in terms of all of the above. It is descending really rapidly and you can see that they’ve had the most amount of millionaires have lost that’s lost in 2025 at an accelerating pace. Poor me, he looks at and goes, what the hell is wrong with these people? Why were they so slow? I was talking about this five years ago. A lot of this is pessimistic in nature or can be. Um I like to prefer to just look at the world as a realist and say, trends are unfolding. I need to understand them and I need to position accordingly. I can’t as a little hedge fund manager influence the outcomes. What I can do is understand them as best as I can and then up my clients accordingly. And there’s a lot of opportunities to come out as a consequence.

Democratic erosion in the West

CHRIS: I mean, you know, as I mentioned, back in gosh 2018, 19, I remember writing a whole report about you need to be putting money into Dubai. And the reasons why. And people like, oh, I don’t want to buy into a dictatorship and I’m like, yeah, you’re not living in anything other than a fucking dictatorship now. You just think that you’re not because there’s a facade around it. That that’s called democracy. And and so like now we The facade is fast unraveling though.

LADISLAS MAURICE: The facade is fast unraveling though.

CHRIS: It is fast unraveling. But here’s the thing, right? Like when you understand that it’s a facade, the arbitrage value between perception and reality is the greatest. That arbitrage value is already been closing, right? Dubai real estate’s up two, three times as a consequence. But it’s still relatively cheap. That trend is continuing to unfold. I’m just using Dubai as an example because it was unbelievably cheap when when we first mentioned it. Now it’s not unbelievably cheap, but on a relative basis, it is still much, much better value than Berlin, Barcelona, Paris, London, New York, Boston, and it has a whole host of benefits. Don’t get me wrong, it’s not like you’re still living in the desert. I don’t I don’t want to live in Dubai. Trust me. But everything becomes relative.

Seeking refuge from Western decline

CHRIS: You know, it’s um I was chatting to a friend this morning and we’re talking about a friend of his and um walking the streets in I can’t remember what part of London. And and then they’d taken a trip over to Dubai and they were like, this is paradise. And I’m like, no, it’s not paradise. It just feels like paradise because you can walk the streets and it’s safe. And you can like wear nice clothing and a watch and not be stabbed for it. That’s what feels now it feels like paradise to you because you’ve slowly been the boiling frog in this other environment that you’ve become accustomed to. And then you step out of it and you’re like, oh my god, I can breathe. That’s the trade that people will increasingly make. And so that arbitrage value still exists. But that’s going to continue as Europe continues down the path that it’s that it’s on. And there’s a number of jurisdictions which will benefit as a consequence.

Southeast Asia where you’ve spent some time is another one. I would say Argentina’s another one too. There’s different risk profiles across all of these places and there’s different probabilities, but these are some of the trends unfolding. So they’re quite easy to identify that here whether you like them or not.

Subscribe to Chris’ newsletter

LADISLAS MAURICE: Look, thanks a lot, Chris. Um Chris has a very interesting newsletter that I’ve subscribed to for a few years. I really recommend people just at least try. Um there’s a 30-day guarantee if you’re not happy, just send Chris an email and say, I want my money back. You get it back. So it really doesn’t really cost you anything to try. There is an affiliate link below with a nice discount. So Chris, thank you very much for your time today.

CHRIS: You’re most welcome. It’s good to see you again, mate.

LADISLAS MAURICE: Make sure to download my free ebook 12 mistakes to avoid when investing in international real estate, which you can find on my website, link below. And feel free to follow me on Instagram @TheWanderingInvestor. I look forward to hearing from you.